-

Never Enough

(swipe right to continue)

-

In March 2023, the Office of National Statistics published its most recent report on housing affordability in England and Wales. The report analyzed the median house prices and median household income to determine the number of times a household salary is required to buy a property. The results were staggering, with the number reaching an all-time high, a situation exacerbated by the lockdown when property prices were inflated due to the pandemic.

-

House Prices to Earnings Ratio Comparison between London and England (2002-2022)

-

In 2002, London's ratio was 6.74 compared to England's ratio of 4.92. By 2022, London's ratio had risen to 13.33 while England's ratio was 8.28. This suggests that the housing market in London is particularly unaffordable in comparison to the rest of England, with house prices rising faster than earnings. The data also suggests that the gap between London's ratio and England's ratio is widening, with London's ratio increasing at a faster pace in recent years.

-

-

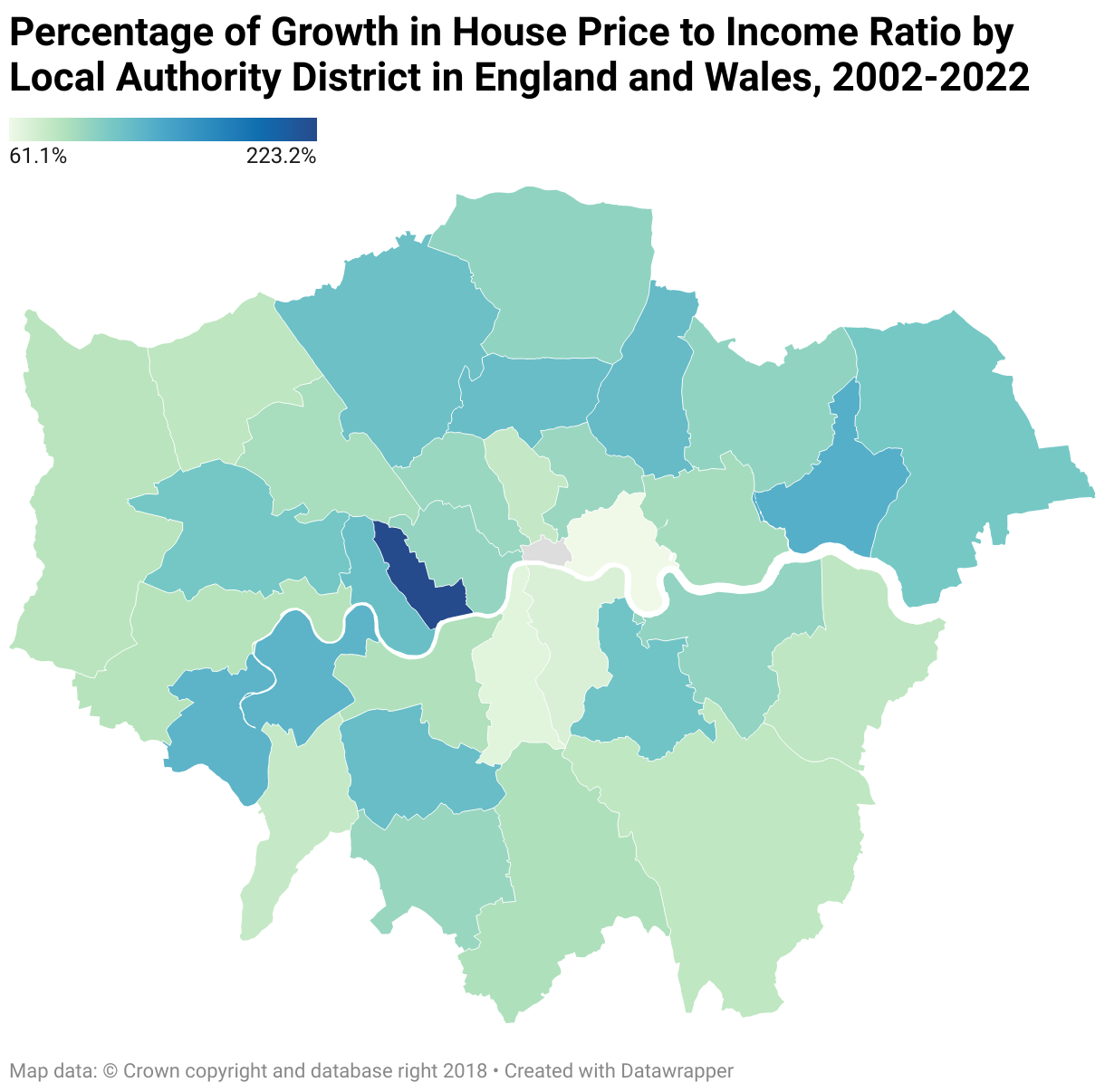

The pandemic restrictions that closed offices and decimated London's hospitality industry have caused many young people to relocate from the city center to the suburbs. The map illustrates the increase in the housing affordability ratio percentage for each borough in London over the years. From the map, we can see the suburban boroughs are witnessing a significant rise in unaffordability.

-

House Price Growth vs Median Income Growth in London

-

From 2003 to 2022, the house price growth in London has consistently outpaced median income growth, with the gap between the two increasing significantly over time. From 2003 to 2008, house price growth ranged from 14% to 56%, while median income growth ranged from 3.83% to 23.23%. From 2009 to 2018, house price growth ranged from 47% to 169%, while median income growth ranged from 26.57% to 41.48%.

The trend continued in the following years, with the gap widening even further. In 2022, the accumulated house price growth was 209%, while the total median income growth was 56.10%, nearly four times less. This comparison indicates a continuing trend of disproportionate growth in London's housing market, with many Londoners unable to keep up with the rising prices despite an increase in wages.